Understanding how much house you can afford is crucial when planning to purchase a home. Many individuals and families find themselves asking, “If I make $70,000 a year, how much house can I afford?” This question not only serves as a financial consideration but also affects long-term stability and lifestyle choices. In this article, we will explore the various factors that go into determining how much house you can afford and provide helpful insights with real data.

If I make $70,000 a year, how much house can I afford?

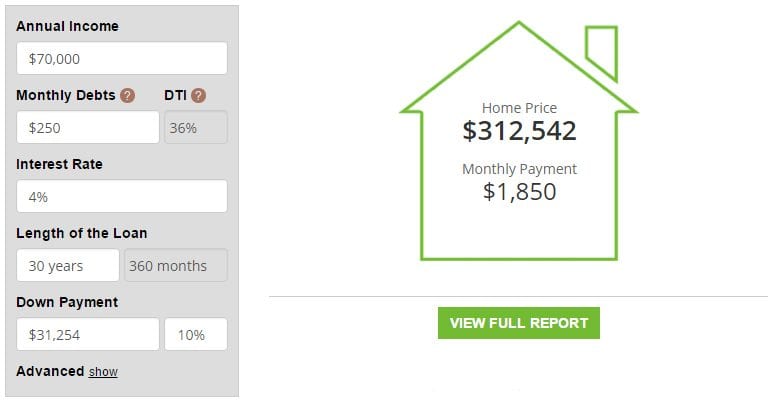

Typically, financial experts recommend that your total housing expenses should not exceed 28% to 30% of your gross monthly income. This means that a household earning $70,000 annually can afford a monthly housing payment ranging from $1,633 to $1,750, depending on various factors such as debt-to-income ratio, down payment, and interest rates.

Breaking Down Your Income

To begin, it’s essential to calculate your monthly gross income. For an annual salary of $70,000, the calculation is fairly straightforward:

- Monthly Gross Income = Annual Salary / 12

- Monthly Gross Income = $70,000 / 12 = $5,833.33

Using the 28% guideline:

- Maximum Monthly Housing Expense = Monthly Gross Income x 0.28

- Maximum Monthly Housing Expense = $5,833.33 x 0.28 = $1,633.33

Using the 30% guideline:

- Maximum Monthly Housing Expense = Monthly Gross Income x 0.30

- Maximum Monthly Housing Expense = $5,833.33 x 0.30 = $1,750.00

This gives a range of approximately $1,633 to $1,750 for your monthly housing expenses.

Factors Influencing Home Affordability

Several elements contribute to how much house you can buy. Below are some of the most significant factors.

- Debt-to-Income Ratio (DTI)

Your DTI ratio reflects how much of your income goes toward debt payments. Lenders generally prefer a DTI under 36%. This means that if your monthly debts amount to $1,800, you can afford a maximum monthly housing expense of about $1,250. - Down Payment Size

The more you put down initially, the less you owe on your mortgage. Common down payment amounts are 5%, 10%, or 20%. A higher down payment will generally allow you to afford more house, as it reduces your monthly mortgage payment. - Interest Rates

Mortgage interest rates fluctuate based on economic conditions. A lower interest rate can significantly reduce your monthly payments, allowing you to afford a more expensive home. - Loan Term

The length of your mortgage affects monthly payments. An adjustable-rate mortgage (ARM) or a 30-year fixed mortgage can influence how much you can afford monthly. - Property Taxes and Homeowners Insurance

Local taxes and insurance costs will vary, impacting your monthly payment. Always include these in your affordability calculations.

Calculating Your Home Price

To determine the price range of a home you can afford, we need to factor in interest rates, loan terms, and down payments.

For instance, let’s say you plan to put down 10% on a home for a 30-year fixed mortgage with an interest rate of 3.5%. Using the monthly payment from earlier ($1,750) and a down payment of $15,000 (10% of a $150,000 home), we can find the home price you can afford.

Using a mortgage calculator:

- Monthly Payment = Principal + Interest + Taxes + Insurance

Assuming that taxes and insurance cost $300 per month: - Subtract these costs from your maximum monthly payment:

$1,750 – $300 = $1,450.

Using this amount to calculate the maximum loan amount with a 3.5% interest rate for 30 years gives a result of approximately $325,000.

Based on the given data, here’s how the calculations could look:

| Criteria | Values |

|---|---|

| Annual Income | $70,000 |

| Monthly Gross Income | $5,833.33 |

| Max Monthly Housing Payment | $1,750 |

| Down Payment | 10% ($15,000) |

| Estimated Mortgage Amount | $325,000 |

Conclusion: Making Informed Decisions

Understanding how much you can afford is critical for a successful home-buying experience. With an annual salary of $70,000, your affordability range will depend on multiple factors, including your debt levels, down payment, interest rates, and financial goals.

Start by assessing your total debt load, consider your down payment options, and review local property costs. Different lenders may offer varying terms, so it’s beneficial to shop around. A financial advisor or mortgage consultant can also help clarify your specific situation.

With the right information and careful planning, you can make a sound investment in your future. Whether you wish to live in the heart of a city, in the suburbs, or a rural area, understanding your financial landscape will guide you in finding the home that fits within your budget.