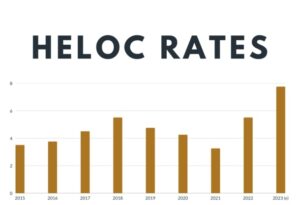

As interest rates decline, many homeowners are turning to home equity lines of credit (HELOCs) for financing, taking advantage of potential cost savings. With an average of $330,000 in home equity, many homeowners now have the opportunity to cover large expenses through this flexible borrowing option. However, the variable nature of HELOC interest rates can make budgeting a challenge, especially as they adjust monthly.

Understanding HELOC Costs

HELOCs offer flexibility, allowing borrowers to draw from a line of credit as needed rather than receiving a lump sum. These loans come with variable interest rates that can fluctuate over time, meaning that while borrowers may benefit from falling rates now, they should also be prepared for potential increases in the future.

Here’s a breakdown of monthly payments on a $75,000 HELOC, based on the average rate of 8.73% as of October 18 and two common repayment periods.

These payments reflect current averages, but what if rates continue to fall? Economists predict further rate cuts of 25 basis points by the Federal Reserve in the coming months. If HELOC rates follow suit, payments could decrease as well. Here’s how the numbers stack up if the average rate drops to 8.48%:

It’s important to note that HELOC rates may not adjust exactly in line with federal rate changes. Additionally, rates can vary depending on borrower qualifications, including credit scores and financial history.

Considering Home Equity Loans

Homeowners should also consider traditional home equity loans, which offer fixed interest rates, making them easier to budget for. Currently, the average interest rate for these loans is 8.36%. While this can be appealing, it also means borrowers may miss out on potential rate cuts unless they choose to refinance.

The Pros and Cons of Each Option

HELOCs offer flexibility and allow homeowners to take advantage of decreasing rates without the need to refinance. However, the variable rates mean that monthly payments could increase unexpectedly. Traditional home equity loans provide stability and predictability, making them ideal for those who prefer fixed payments, even if it means potentially refinancing later to secure a lower rate.

What Homeowners Should Know?

For those considering a $75,000 HELOC, the expected monthly payments range from approximately $749 to $939. While rates are currently declining, there’s always a chance they could rise again, so homeowners should carefully evaluate their budgets and potential rate scenarios. Remember that your home is used as collateral in both HELOCs and home equity loans, meaning failure to repay could lead to foreclosure.

Ultimately, borrowers must understand their financial situation and choose the product that best suits their needs, whether that means taking advantage of the flexibility of a HELOC or the predictability of a home equity loan.